_______

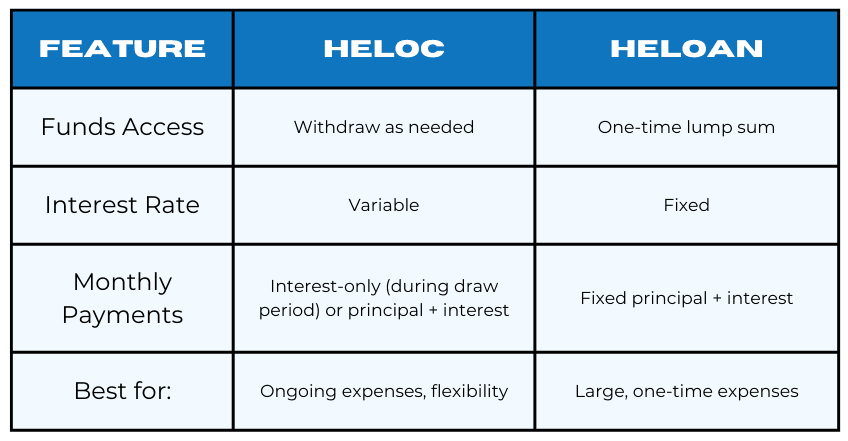

Revolving Credit Line: Borrow as much or as little as you need, up to your approved limit.

_______

Variable Interest Rates: Rates can fluctuate based on market conditions.

_______

Draw Period & Repayment Period: Typically, you can borrow for 5-10 years (draw period) and then repay over 10-20 years.

_______

Interest-Only Payments: During the draw period, you may have the option to make interest-only payments, keeping monthly costs low.